As contractors and real estate developers plan for 2026 and beyond, recent changes under the OBBBA deserve close attention. The updates significantly expand which residential construction projects can defer income recognition for tax purposes. For businesses operating on long build cycles, the result can be a substantial timing difference that improves cash flow and reduces taxable income in earlier years of a project.

For many firms, these changes represent a shift from rules that historically accelerated tax obligations well ahead of actual cash collection.

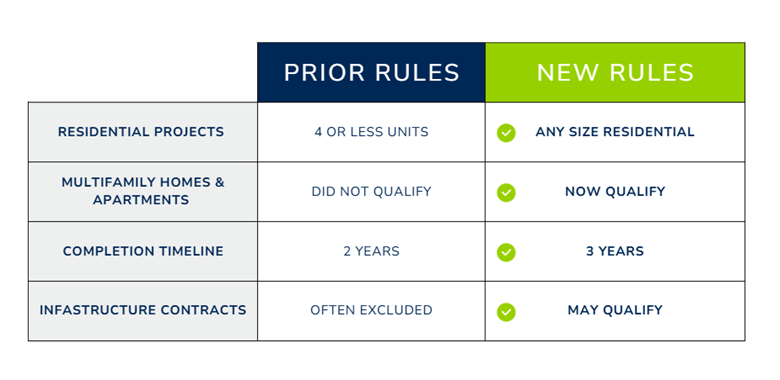

Where the Old Rules Fell Short

Under prior law, relief from the percentage of completion method was limited to a narrow category known as “home construction contracts.” To qualify, at least 80 percent of total estimated contract costs had to relate to dwelling units in buildings with four or fewer units. While the rule worked for single-family and small residential projects, it excluded much of today’s residential development activity.

Apartment complexes, multifamily housing, senior living facilities, student housing, and mixed-use projects typically failed the four-unit test. Contractors on these projects were often required to recognize income as work progressed, even when retainage, financing structures, or phased billing delayed payment. In some cases, taxes were owed years before the project generated meaningful cash.

A Broader Definition Changes the Playing Field

The OBBBA replaces “home construction contracts” with a broader definition of “residential construction contracts.” The four-unit limitation has been eliminated. Projects involving residential rental or ownership buildings may now qualify regardless of scale.

This expansion is particularly impactful for contractors working on multifamily developments. It also applies more broadly than many realize. Contractors performing site work or infrastructure improvements such as roads, utilities, sewer, or water systems for residential developments may also qualify for deferral if their contract relates to a qualifying residential project.

The takeaway is simple. Eligibility is no longer limited to the general contractor or vertical builder. Each contract should be reviewed on its own terms, project by project, and year by year.

More Time to Complete Qualifying Projects

The legislation also extends the expected completion window for qualifying contracts. Under prior law, contracts generally had to be expected to finish within two years to qualify for exemption from the percentage of completion method. That window has now been expanded to three years.

This added time is meaningful for larger residential developments that previously fell just outside the two-year threshold. It provides greater flexibility for projects with phased construction, financing delays, or regulatory hurdles that extend timelines beyond initial estimates.

Why Income Timing Matters

When a contract qualifies as a residential construction contract, contractors may be able to use the completed contract method or, in some cases, the cash method for tax reporting. Compared to percentage of completion, these methods allow income recognition to occur later in the project life cycle.

The practical effect is better alignment between taxable income and actual cash received. This can ease working capital strain, reduce borrowing needs, and lower current-year taxable income during construction years. Over long build cycles, the cumulative cash-flow benefit can be significant.

Additional updates reinforce this shift. The look-back method no longer applies to residential construction contracts entered into in tax years beginning after July 4, 2025. The AMT percentage of completion exemption has also been expanded to include residential construction contracts, aligning alternative minimum tax treatment with regular tax rules.

Planning Considerations as 2026 Approaches

These changes create opportunity, but they also require careful review. Contractors and developers should consider evaluating active and upcoming projects to determine which contracts may qualify under the new definition. In some cases, changing tax accounting methods may be appropriate, which could involve filing Form 3115. Further guidance is still expected, making early analysis even more important.

While the rules do not change the total income recognized over the life of a project, they do change when that income is taxed. For many construction and development businesses, timing is everything.

As residential construction continues to evolve, proactive planning can help ensure these rule changes work in your favor. If you have questions about how the updated definitions or timelines apply to your projects, a conversation now can help position you well for the years ahead.